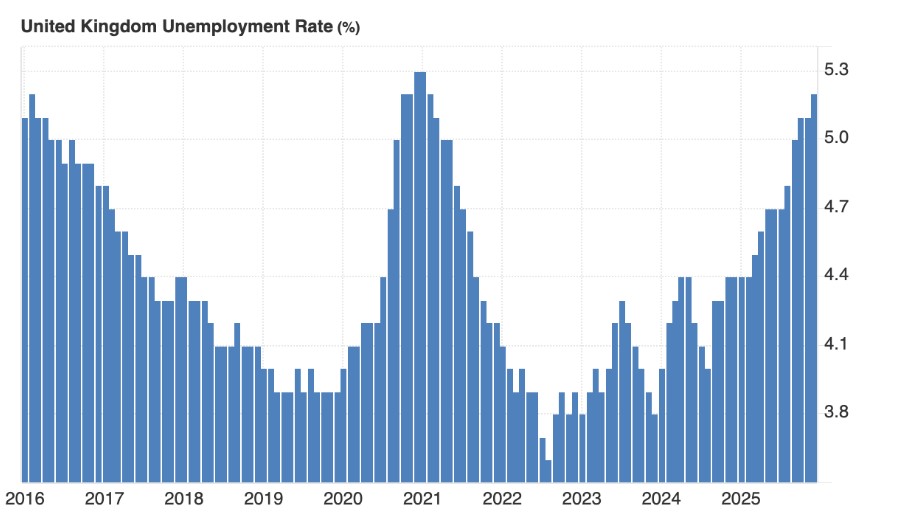

Recent labour market figures from the United Kingdom have sparked renewed speculation that the Bank of England (BoE) may implement multiple interest rate cuts in 2026. The latest data showed a significant softening in the jobs market, with the unemployment rate rising to approximately 5.2%, marking the highest level in several years. At the same time, wage growth has slowed considerably, particularly in the private sector, reducing inflationary pressures linked to labour costs. Payroll figures also declined for the fifth consecutive month, suggesting a broader slowdown in employment growth.

Financial markets have reacted swiftly to these developments. Investors now anticipate as many as three separate rate reductions throughout the year, beginning potentially as early as the BoE’s March policy meeting. Current forecasts suggest the central bank’s base rate, presently at 3.75%, could fall to around 3.00% by the end of 2026 through incremental 0.25 percentage point cuts. The anticipated easing reflects expectations that the BoE will act to support a cooling economy and ensure continued economic stability.

The potential rate cuts carry implications for both households and the broader economy. For mortgage holders, lower base rates could translate into reduced borrowing costs, offering opportunities for refinancing or securing more affordable loans. Conversely, savers may face lower returns on savings accounts and fixed-rate investments. From a macroeconomic perspective, reduced interest rates are intended to stimulate investment, encourage spending, and ultimately support job creation in sectors affected by the labour market slowdown.

This scenario highlights the delicate balancing act faced by central banks, which must weigh inflation control against the need to sustain economic growth and employment. In the UK, where inflation has recently moderated, the weakened jobs market provides the BoE with both the justification and the necessity to consider a more accommodative monetary policy stance.

UK’s latest jobs figures have not only revealed signs of economic cooling but have also shifted market expectations toward multiple interest rate cuts in 2026. If these predictions hold, households, investors, and policymakers alike will need to adjust to a landscape of cheaper borrowing, slower wage growth, and measures aimed at stabilizing economic activity. The situation underscores the importance of timely and measured policy responses in safeguarding economic stability while supporting employment.